Direct Answer: A Credit Privacy Number is a nine-digit number that is often marketed as an alternative identifier for consumers seeking to separate certain financial activities from their Social Security Number. Before using any Credit Profile Number, consumers should understand how they work, what legal limitations exist, and why credit education is critical when building a financial profile.

Most people never think about their credit profile until they need it. Maybe you’re applying for an apartment, trying to finance a vehicle, opening a utility account, or simply looking for ways to rebuild after financial challenges. That’s often when people first hear the term Credit Privacy Number and begin searching for answers.

The problem is that there is a lot of misinformation online. Some websites make unrealistic promises, while others fail to explain the concept clearly. This guide will help you understand the basics, explore common questions, and learn what to consider before moving forward.

What Is a Credit Privacy Number?

A Credit Privacy Number is commonly described as a nine-digit identifier used for credit-related purposes. Many consumers become interested in Credit Privacy Numbers after experiencing identity theft, privacy concerns, credit reporting issues, or major life changes such as divorce or bankruptcy.

In simple terms, a CPN Number is often marketed as a tool that helps establish a separate credit profile. However, it is important to understand that the Social Security Administration (SSA) is the only government agency authorized to issue Social Security Numbers.

According to the Social Security Administration, individuals cannot legally create or invent a replacement Social Security Number. Consumers should always ensure that any financial activity complies with federal, state, and local laws.

Quick Comparison

| Feature | Social Security Number | Credit Privacy Number |

|---|---|---|

| Issued by Government | Yes | No |

| Used for Taxes | Yes | No |

| Used for Employment Verification | Yes | No |

| Used for Federal Benefits | Yes | No |

| Often Used for Credit Profile Building | No | Yes |

| Legal Restrictions Apply | Yes | Yes |

Why Do People Look for a Credit Privacy Number?

There are many reasons someone may research a Credit Profile Number.

Some of the most common situations include:

- Identity theft concerns

- Privacy-related issues

- Credit rebuilding efforts

- Recent divorce

- Bankruptcy recovery

- Thin or limited credit history

- Starting fresh after financial setbacks

- Apartment application challenges

For many people, the goal isn’t necessarily to avoid obligations. Instead, they’re looking for ways to rebuild, organize, and improve their financial situation.

The key is understanding what a Credit Privacy Number can and cannot do.

How Does a Credit Privacy Number Work?

A Credit Privacy Number is generally used alongside credit-building strategies designed to establish and strengthen a financial profile over time.

These strategies may include:

- Authorized user tradelines

- On-time payment history

- Responsible credit utilization

- Credit monitoring

- Financial education

- Identity protection practices

A Credit Profile Number alone does not automatically create a high credit score.

Just like any credit profile, positive reporting history and responsible financial behavior are major factors in long-term success.

According to the Consumer Financial Protection Bureau (CFPB), payment history and credit utilization remain among the most influential factors in many credit scoring models.

Is a Credit Privacy Number Legal?

This is one of the most frequently asked questions.

The answer depends on how the Credit Privacy Number is used.

Consumers should understand several important points:

- A Credit Profile Number is not issued by the Social Security Administration.

- A Credit Profile Number cannot legally replace a Social Security Number for tax purposes.

- A Credit Profile Number should not be used to misrepresent identity.

- Federal laws prohibit providing false information on credit applications.

The Federal Trade Commission (FTC) has published warnings regarding companies that falsely claim consumers can legally replace their Social Security Numbers.

Before using a CPN Number, consumers should conduct thorough research and seek professional guidance when appropriate.

What Is the Difference Between a Credit Privacy Number and an SSN?

Many beginners confuse these two identifiers.

Here’s a simple breakdown:

| Credit Privacy Number | Social Security Number |

|---|---|

| Not issued by SSA | Issued by SSA |

| Used in certain credit-building strategies | Required for taxes and employment |

| Cannot replace SSN for government purposes | Primary federal identifier |

| Often associated with credit privacy services | Used for federal reporting |

Understanding this distinction is extremely important.

One of the biggest mistakes consumers make is assuming the two are interchangeable. They are not.

Who Typically Uses a Credit Privacy Number?

People from many different backgrounds explore Credit Privacy Numbers.

Examples include:

Consumers Recovering From Financial Hardship

Life happens. Medical debt, divorce, job loss, and unexpected emergencies can negatively impact credit.

Many consumers begin researching a Credit Profile Number while searching for ways to improve their financial future.

Identity Theft Victims

According to the Federal Trade Commission, identity theft remains one of the most reported consumer fraud categories in the United States.

Victims often become more focused on privacy and credit monitoring.

Individuals With Limited Credit History

Young adults and consumers with thin credit files sometimes seek additional educational resources regarding credit-building strategies.

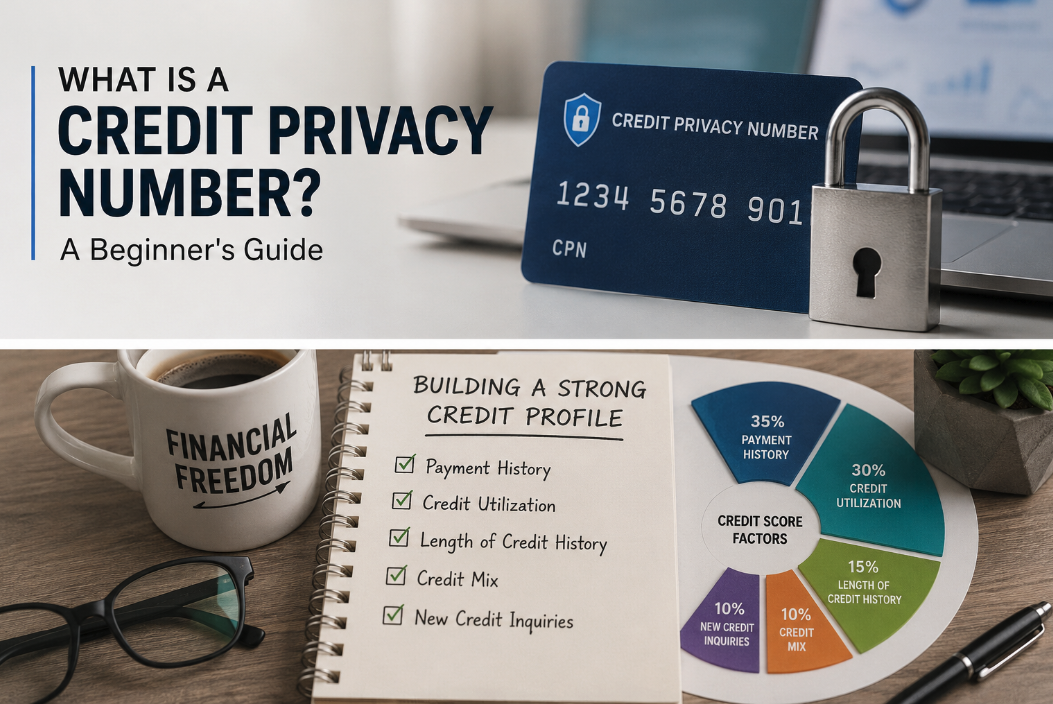

What Factors Affect Credit Scores?

Whether someone is using traditional credit-building methods or researching about CPN Numbers, understanding credit scoring fundamentals is critical.

Major Credit Score Factors

| Factor | Approximate Impact |

|---|---|

| Payment History | 35% |

| Credit Utilization | 30% |

| Credit Age | 15% |

| Credit Mix | 10% |

| New Credit Inquiries | 10% |

Source: Fair Isaac Corporation (FICO)

This table highlights an important reality:

No number by itself creates a strong credit profile.

Positive credit behavior is what ultimately drives long-term results.

What Are Common Misconceptions About a Credit Privacy Number?

There are several myths that continue to circulate online.

Myth #1: A Credit Privacy Number Automatically Creates Good Credit

False.

Credit scores are built through reporting history, utilization, payment patterns, and other factors.

Myth #2: A Credit Privacy Number Replaces an SSN

False.

The Social Security Administration remains the sole issuer of Social Security Numbers.

Myth #3: A Credit Privacy Number Guarantees Approval

False.

Lenders evaluate many variables, including income, debt levels, credit history, and underwriting standards.

Myth #4: A Credit Privacy Number Eliminates Past Debt

False.

Existing legal financial obligations do not simply disappear.

What Should Beginners Look for When Researching a Credit Privacy Number?

If you’re considering learning more about a CPN Number, focus on education first.

Ask these questions:

- Is the company transparent?

- Are legal limitations clearly explained?

- Are there realistic expectations?

- Is there ongoing customer support?

- Are credit-building strategies discussed?

- Is identity protection addressed?

A reputable organization should prioritize education over exaggerated promises.

How Long Does It Take to Build a Credit Profile?

Credit building is typically a process, not an overnight event.

While timelines vary, many consumers focus on:

- Establishing reporting accounts

- Maintaining low utilization

- Monitoring credit activity

- Making payments on time

- Avoiding excessive inquiries

Consistency often produces better results than quick-fix approaches.

According to Experian, credit improvement timelines can vary significantly depending on an individual’s starting point and overall financial behavior.

Frequently Asked Questions About Credit Privacy Number

What is a Credit Privacy Number used for?

A Credit Privacy Number is commonly marketed as an identifier used in certain credit-related strategies and privacy-focused financial services.

Is a Credit Profile Number the same as an SSN?

No. A Credit Privacy Number is not a Social Security Number and cannot replace one for tax, employment, or federal purposes.

Can a Credit Profile Number guarantee loan approval?

No. Lenders consider many factors beyond identifiers, including income, credit history, debt ratios, and underwriting requirements.

Can identity theft victims use a Credit Profile Number?

Many identity theft victims research privacy-related credit solutions, but they should always seek professional guidance and verify compliance with applicable laws.

How long does credit building take?

Timelines vary based on credit history, utilization, payment behavior, and overall financial circumstances.

Does a Credit Profile Number create a credit score automatically?

No. Positive reporting history and responsible credit management are necessary to establish and maintain a credit profile.

Should I research the company offering Credit Profile Number services?

Absolutely. Transparency, education, and compliance should always be top priorities.

Final Thoughts on Credit Privacy Numbers

A Credit Profile Number continues to be a topic that generates significant interest among consumers seeking privacy, credit education, and financial rebuilding strategies.

The most important takeaway is this: a Credit Profile Number should be viewed as one part of a larger financial picture. Understanding credit scoring, maintaining responsible financial habits, and working with reputable organizations are often more important than any single tool or strategy.

Before making any decision, take the time to educate yourself, review authoritative resources, and ensure that any approach aligns with applicable laws and best practices.